Company: ChargePanel

Ticker: $CHARGE

Website: https://www.chargepanel.com/

Industry:

ChargePanel specializes in the management, operation and usage of Electric Vehicle Charge Points.

We provide adaptable solutions for charge point owners, resellers and organizations.

Pre money valuation: 7,78 MUSD or 71 MSEK

IPO offering size: 2,73 MUSD or 24,9 MSEK

IPO signup period: 16-30th of November.

IPO date: The first trading day is anticipated to be 9th of december 2021 at First North

Prospectus: https://www.chargepanel.com/sv/ir/detaljer-ipo/

IPO price: 0,65 USD or 5,9 SEK

Target price (link): Analyst group has put a (what ESGFIRE thinks is a conservative) target price of 0.94 – 1,13 USD or 8,5-10.2 SEK in a Base / bull Scenario.

ESGFIRE reasons for subscribing for shares in the IPO of Chargepanel:

We have chosen to subscribe for a large position in the ongoing Initial public Offering (IPO) of the company Chargepanel. Chargepanel is a Software as a Service company (SaaS) operational in software as a service, fleet management and electric vehicles. We think this is a fantastic business combination which we think is perfectly positioned for massive growth. Seeing as 71 % of the IPO offering has already been signed for by subscription commitment there is most likely not many shares available for the public. Below we will give a brief background of the company, business models, growth plans, financial projections, risk scenarios and finally subscription / trading information.

Background and IPO details

Chargepanel is a Swedish company that provides Saas (software as a service) for electric vehicle charging. In summary ChargePanel simplifies EV charging and EV fleet management for both EV users, chargestation owners and corporations that own/offer charging stations for their clients/employees. The company is currently operating in Sweden, Norway and the United Kingdom and has a growth plan which aims to establish a presence for the company in all parts of the world before 2025, not a modest ambition! The business concept is to offer white label solutions to companies who want to be a part of the growing EV charging infrastructure market for electric vehicles. The company aims to grow globally with their existing partners . The global electric charging station market is expected to reach $20.49 billion in market value by 2025 at a compounded annual growth rate of 31.8%. The number of charging stations worldwide is meanwhile projected to grow with a compounded annual growth rate of 92 % until 2025.

The internal corporate goals for Chargepanel is to reach a turnover of 17,55 MUSD or 160 MSEK by 2024. The research firm Analyst Group projects that the company will have reached 5 new markets by 2024 and grow with a compounded annual growth rate of 49 % between 2020-2024.

The management of the company estimates that the company would be profitable even without the capital from the ongoing IPO however capital is needed for the company’s growth plan which is why the IPO is being done.

The money from the IPO is aimed to be used as follows:

45 % hiring of new staff for expansion and sales

30 % marketing of the SaaS platform in chosen markets

15 % operating expenses

10 % financial buffer

Product concept

Chargepanel uses an Open Charge Point Protocol (OCPP), which means their software service can be integrated with different types of hardware (charging stations) from different suppliers. This can be controlled from the same backend system. OCPP used by Chargepanel is the standard communication between backend and charging stations and is currently implemented in 78 countries worldwide. Chargepanel’s platform is also connected to a global E-roamingnetwork. The E-roamingnetwork can be described as the equivalent of the internet roaming feature within the European Union where different operators open their grid for each other’s customers. For the end customer this is a huge advantage since they therefore can connect to any charging station without the need for different applications and/or RFID tags. Using E-roaming the end client only needs ONE account at ONE operator to use the entire network. Chargepanels has partnered with Hubject which runs the biggest global E-roamingnetwork with more than 250 000 charging stations connected in 43 countries. For the end client it can be mentioned that Chargepanel has three different applications, “Enterprise” which is the complete white label system for EV charging networks, “Cloud” which is the owner system for charging operators and “Connect” which is the mobile application for EV users. In summary, chargepanel simplifies EV charging and EV fleet management for both EV users, chargestation owners and corporations that own/offer charging stations for their clients/employees. For a Complete detailed feature of the service offering check out Chargepanels website which is very informative and available both in English and Swedish. Direct link is available HERE.

Business model and revenue streams

Chargepanel has developed a well diversified revenue stream of three different types of subscription services. The subscription services are based on the different segments where their Business to business clients (B2B) are operating. These subscription models are as follows:

1. Business to business clients using the chargepanel platform in the form of a starting fee and a monthly subscription fee.

2. A revenue fee for every charging socket that the client connects to Chargepanel.

3. Other revenues such as optional value adding services in the form of Fleet management and shares of different transaction fees.

The majority of revenues today are one off revenues connected to installing the platform. It is most likely, just as Analyst group predicts, that the recurring subscription revenues will be the majority of revenues down the line.

Scalability, profit and evaluation.

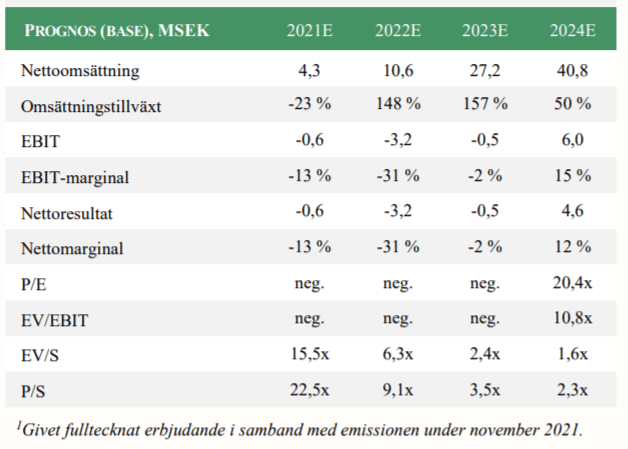

Since the company uses a SaaS-business (Software-as-a-Service) model they can grow their business exponentially and with high scalability without radically increasing their costs. The research firm Analyst Group projects the company will reach break even by 2023 and an EBIT margin of 15 % by 2024. For 2022 the company is valued at a Price to sales of 6.3 . Analyst Group states that Chargepanel based on 2023 figures is , based on their IPO evaluation, considerably lower valued at EV/Sales of 2,3 compared to a 9.3 multiple for their peer group.

The Base scenario financial projections from the research firm Analyst group are shown below in SEK. We note that Analyst Group for some reason are extremely conservative in their projections as they differ very much from the company’s own projections. For example the company projects revenues of 17,55 MUSD or 160 MSEK by 2024 and Analyst group only projects 4,5 MUSD or 40,8 MSEK by 2024 which is a staggering 75 % lower than the company’s own projection. Even by using these extremely conservative numbers the research firm Analyst group has a bull case scenario target price which is almost 100 % above the IPO price of Chargepanel.

Risks to consider

The biggest risk, according to Analyst Group, is an extended global shortage of semiconductors which can affect the purchasing power of their clients and in turn the initial growth rate of Chargepanel significantly. A lower growth rate than anticipated of the electric vehicles sector could also cause a delay in revenues for Chargepanel. Other risks that ESGFIRE notes is the dependence of key personnel, and the possibility of more rapidly growing competitors.

Trading and where to sign up

Chargepanel is aiming to commence trading on the Swedish Nasdaq First North on december 9th of 2021. You can sign up for shares either through online brokers Avanza, Nordnet or using BankID. The minimum investment is 585 USD or 5310 SEK. The final date for share subscription is 30th of november 2021.

Legal Disclaimer

We may on the date of the IPO own shares of this company personally.

Investing in stocks is combined with certain risks and it is possible to lose your entire investment. Our posts are made for Educational purposes only and are not to be interpreted as tips , financial advice or recommendations of any kind to either buy or sell any stocks.

Companies may or may not be paying us for content posted on this blog.