Originally published on 10/7 2026

ESGFIRE returns since 2018: + 1000 %

Don’t forget to subscribe to our newsletter since that is our main point of contact with our readers.

Click this link to sign up for our free newsletter!

How to read this report

-Market – what is happening and why – provides the macro backdrop

-What is driving capital flows – summarises key market drivers

-Takeaways – outlines how we are positioning

-ESGFIRE Public Portfolio – covers updates across current holdings

-Non Public investment portfolio – shows our private investments

-Watchlist – includes companies we monitor for potential entry

Market – What is happening and why

June broke the two-month winning streak – and the break came from the exact place that had been leading.

After a powerful April–May run, the tape wobbled in June. The S&P 500 slipped roughly 1% on the month and the tech-heavy Nasdaq fell about 2.8%, as investors began to question whether the AI leadership had run too far, too fast. The rotation was stark: Microsoft dropped around 17% (its worst month since 2000) and Oracle fell about 35% (its worst since 1990), while the Dow actually rose about 2.5% as capital moved into financials, healthcare and industrials. Underneath, semiconductor and memory names kept the market from unravelling – the semiconductor complex has surged roughly 88% since March on the AI-infrastructure buildout. Even with the June swoon, the S&P 500 and Nasdaq still closed out their strongest quarter since 2020.

The policy backdrop turned decisively less friendly. At Kevin Warsh’s first meeting as Fed Chair on June 17, the FOMC held the policy rate at 3.50%–3.75% (a 12–0 vote), stripped the easing bias out of a deliberately “curt” statement, and dropped forward guidance entirely. The updated dot plot moved the median year-end rate to 3.8%, with nine of eighteen participants now penciling in at least one hike in 2026. The committee raised its inflation projections (to 3.6% headline / 3.3% core PCE), trimmed growth to 2.2% and nudged unemployment to 4.3%. With May CPI at 4.2% headline (2.9% core), the “last mile” of disinflation looks harder, not easier, and markets sold off on the day.

The one genuinely disinflationary force in June was energy. As U.S.–Iran ceasefire and memorandum-of-understanding hopes built, crude unwound much of its war premium: Brent fell to its lowest since early March mid-month and WTI briefly closed below $70 for the first time since late February, before a late-June flare-up of tit-for-tat strikes around the Strait of Hormuz pulled prices partway back toward the low-$70s. The message: energy has swung from tailwind to swing factor, but it remains volatile and headline-driven.

In our view, June reinforced – and then stress-tested – the thesis we have carried all spring: this is an execution-driven market, not a liquidity-driven one. When even mega-cap AI names can lose a fifth of their value in a month because the story briefly outran the near-term numbers, the premium on hard, disclosed proof points only goes up.

Within sustainability investing, the transition continues to be carried by:

-energy security

-domestic supply chains

-industrial competitiveness

-electrification

-critical minerals

infrastructure buildout

The market is still rewarding builders over storytellers – and June was a reminder that the market will re-rate even the crowd favourites the moment execution and valuation drift apart.

Looking into July, we expect:

1.Continued separation between companies posting real revenue, backlog, contracts and financing progress and those still selling a narrative

2.A higher-for-longer rate regime that keeps rewarding self-funded balance sheets and punishing companies dependent on fresh equity

3.Persistent energy and geopolitical noise keeping commodities and defensive positioning relevant

4. Capital still concentrating in AI infrastructure, power, storage, critical minerals and the industrial transition – but with more discrimination on price

For investors, the widening gap between fundamentals and sentiment in the small-cap space is exactly where patient capital tends to find its edge.

What is driving capital flows

Large-cap vs small-cap dispersion:

The dispersion story took a new twist in June. For two months the largest AI names had supplied essentially all of the leadership; in June that same cohort took the hit, with Microsoft and Oracle posting historic monthly drawdowns while semis and memory held the line. Capital briefly rotated toward the more defensive corners of the large-cap complex (financials, healthcare, industrials). Smaller-cap growth and transition companies stayed exactly what they have been all year: selective bets, rewarded only where they put hard numbers – contracts, commissioning, financing, exploration results – on the tape.

Rates & liquidity:

Warsh’s first FOMC removed the cutting bias, killed forward guidance, and left the median dot pointing to a possible hike rather than a cut in 2026. Sticky services inflation and still-elevated goods prices keep the disinflation “last mile” open. The practical consequence is sharper than a month ago: financing conditions now clearly favour companies with capital discipline and existing liquidity, and penalise those reliant on new equity in a selective window.

Inflation & jobs:

May CPI printed 4.2% headline with 2.9% core, and the Fed lifted its own year-end inflation forecasts. Growth was marked modestly lower and unemployment slightly higher. The read-through is a resilient-but-uncomfortable macro: firm enough to keep the Fed hawkish, hot enough on prices to keep cuts off the table.

Energy & commodities:

Oil reversed much of its Iran-war premium through June on ceasefire optimism, with Brent hitting multi-month lows before a late-month rebound on renewed Gulf-shipping tension. Structurally, the UAE’s exit from OPEC (in May) and reported friction with Iraq add supply-side uncertainty. Critical minerals and industrial metals stayed strategically in focus as governments keep prioritising domestic supply-chain security.

Geopolitics & policy:

The Gulf remained the dominant geopolitical variable, feeding directly into the oil-and-inflation narrative and into rate expectations. Trade fragmentation and industrial-policy competition between major economies continued to anchor investor themes, with North American and European governments still backing domestic manufacturing, energy infrastructure and strategic resources.

Sustainability & policy angle:

The transition is still being framed through competitiveness and energy security rather than climate policy alone – and June sharpened the “power demand” leg of that story. AI data-centre and grid-resilience demand keeps pulling capital toward power, storage and critical-materials supply chains. It is worth noting that, per U.S. EIA data cited across the sector this quarter, solar represents over half of all planned U.S. utility-scale capacity additions in 2026 (roughly 43 GW planned this year alone) – the single largest share of any source. Several of our holdings and watchlist names positioned explicitly against that backdrop in June, from UHP industrial gases for semiconductors to distributed-generation solar and battery systems.

Takeaways for investors

– June proved the “numbers over narrative” rule the hard way:

When Microsoft and Oracle can shed 17% and 35% in a single month on nothing worse than “the story got ahead of the returns,” the lesson for the rest of the book is unambiguous. We continue to anchor entry and conviction to disclosed proof points – contracts signed, facilities commissioned, programs launched, first sales recognised – rather than roadmaps.

– Financing visibility is now a primary screen, not a footnote:

With the Fed’s easing bias gone and a hike back on the table, the equity window stays selective. The ability to fund the next 12–18 months without forced dilution has become a core part of every thesis. Closed facilities, non-dilutive grants and disciplined capital structures are doing real work in our process.

– The fundamentals-vs-sentiment gap in small caps widened again:

Several names delivered genuinely strong operational news in June – a first-sale-to-multi-year-contract conversion, a pellet plant commissioned, an exploration program mobilised, a 125 MW solar portfolio acquired – and still traded flat-to-soft as the broader tape wobbled. For patient capital, that disconnect is precisely where asymmetric setups form.

– Stay aimed at the real-economy, “solutions” transition:

The strongest structural pull again came from industrial gases, critical minerals, distributed renewables, electrification, RNG and AI-adjacent power infrastructure. We keep prioritising companies solving concrete operational problems for paying customers – builders over storytellers.

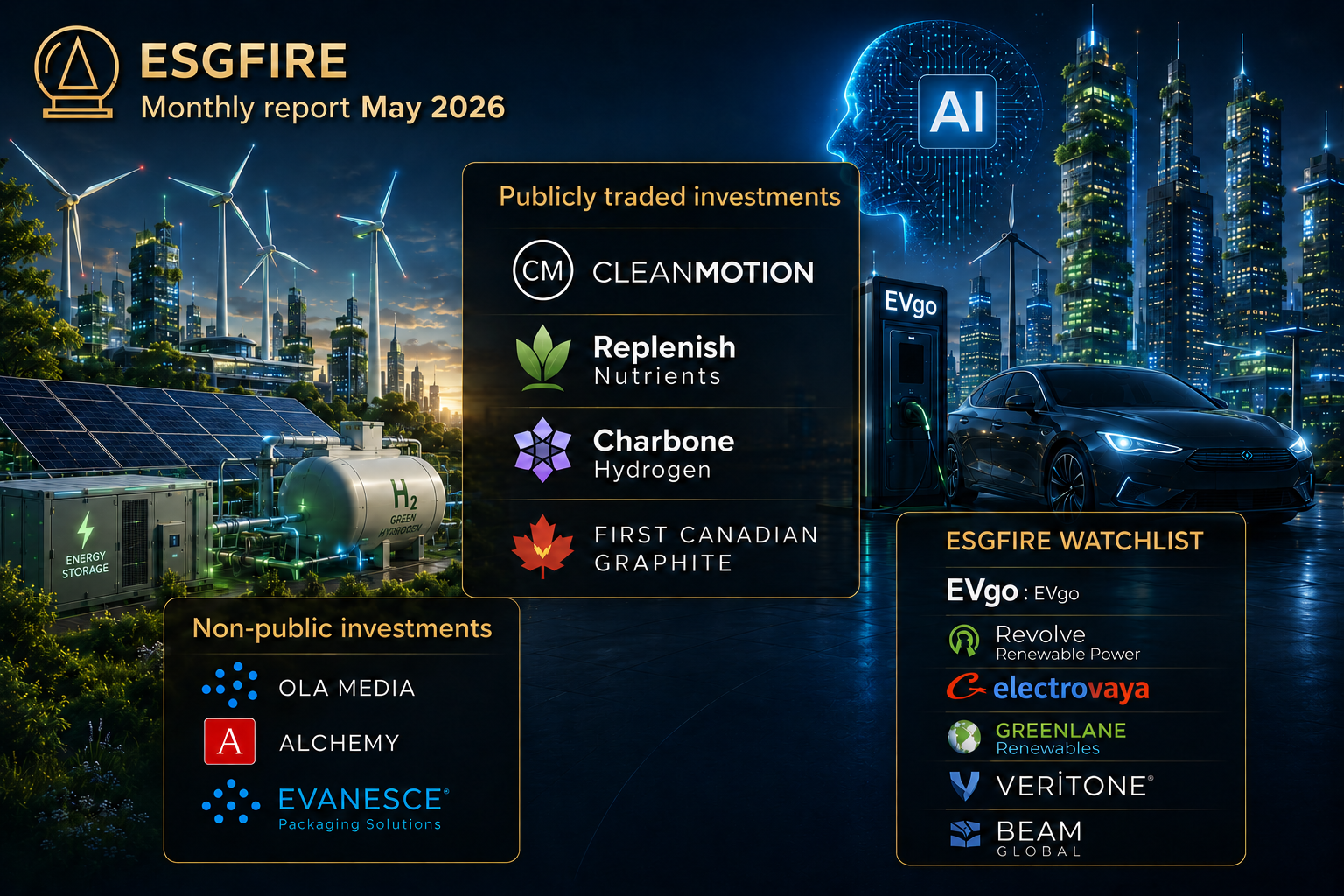

ESGFIRE Public Portfolio – Updates and important events

Clean Motion (Public EV Manufacturer First North: CLEMO)

Key June developments:

-4–6 June: Clean Motion exhibited EVIG Memorial together with Bestattung Wien at the BEFA Forum in Düsseldorf – the leading international funeral trade fair (held every four years, ~230 exhibitors and 10,000+ trade visitors from 40+ countries). The showing pushed the funeral-transport vertical directly into the German, Austrian and Swiss markets and reinforced the recently launched extended-length EVIG Memorial for coffin transport.

-Late June: Clean Motion joined the Wavecomps composite-recycling project, funded by Vinnova and coordinated by RISE (consortium also includes Podcomp, DIAB and Luvly). Total project funding is SEK 4,951,900, of which Clean Motion’s share is SEK 813,000; the project runs June 2026 to January 2029. It targets repurposing the composite sandwich panels already used in EVIG into structural components and storage units – aiming for at least a 50% cut in material waste, a 30% reduction in virgin raw-material use and a 20–35% lower climate impact. CTO William Collings framed it as keeping EVIG’s own materials in a circular loop.

Replenish Nutrients (Regenerative fertilize CSE: ERTH)

Key June developments:

-19 June: Replenish held its Annual General Meeting; shareholders approved all matters put to them.

-24 June: Replenish completed commissioning of its patented pellet fertilizer facility at the Beiseker Hutterite Colony. The line is guided to produce at least 1,000 tonnes per month from Q3 2026 (beginning July), at roughly $600 per tonne and 25–35% gross margins that management expects to flow directly to the bottom line. CEO Neil Wiens described the facility as the first of many Hutterite-colony partnerships and “a foundational step toward building a scalable regenerative-fertilizer platform for large-acre commercial agriculture.”

ESGFIRE view (updated):

The June 24 commissioning converts the capital-light colony model from slide to steel. Stacked with the core Beiseker granulation line (scaling toward its 2,000 tpm target) and the FUE and MJ Ag licensing facilities, Q3 2026 is shaping up as the quarter in which multiple discrete revenue streams converge for the first time. On the company’s own disclosed unit economics, the combined platform capacity sits well above where the equity is currently priced – before assigning any value to the colony-replication and licensing optionality we believe is the real prize (these are ESGFIRE estimates, not company guidance). We continue to watch conversion: tonnage, licensing revenue, and proof that the 24-hour ramp scales on schedule.

Charbone Hydrogen (Green Hydrogen Producer TSX venture: CH )

Performance – June 2026: We are not publishing a precise month-open/close figure as we could not verify clean prints across the month. (Insert exact CH open/close if desired.)

Key June developments:

-4 June: Charbone published a positioning piece on the ultra-high-purity (UHP) industrial-gas supply gap, framing its move to a vertically integrated, demand-driven industrial-gases platform.

-10 June: Charbone signed a long-term hydrogen supply contract with Hone Inc., formalising and extending the Ontario relationship first disclosed on 22 January 2026. Hone deploys mobile hydrogen power (trailer-mounted 165 kW hydrogen ICE gensets that replace ~1,400-amp diesel units) for film and TV production; each generator-day can displace more than 1.5 tonnes of CO₂ versus diesel.

-16 June: Charbone announced 22 new helium customers across Quebec – spanning advanced manufacturing, welding and metal processing, laboratories and specialised technical services – scaling the Helium division it launched in 2025. Chairman & CEO Dave Gagnon called it confirmation of the diversification strategy.

ESGFIRE view (updated):

June turned Charbone’s platform narrative into repeatable commercial evidence: a first-sale-to-multi-year-contract conversion (Hone) and a double-digit jump in helium customers in a single announcement. Anchoring UHP gases to demand that grows regardless of the hydrogen-policy cycle – semiconductors, AI/data centres, pharma, defence, and now on-set film power – remains strategically smart. The caveat is unchanged and central: this is a capital-intensive buildout, and dilution and balance-sheet risk remain the things to watch alongside the demand pull into Phase 1B.

First Canadian Graphite (natural graphite mining TSX venture FCI)

Key June developments – the catalyst month the thesis needed:

-2–4 June: Management held one-on-one investor meetings at THE Mining Investment Event in Quebec City.

-11 June: The company announced participation in Planet MicroCap Las Vegas, with CEO John LaGourgue presenting on 17 June.

-16 June: First Canadian Graphite launched its 2026 Lac Guéret South exploration program – a two-phase surface campaign targeting high-priority electromagnetic (EM) anomalies identified in the May 20 heliborne survey, feeding a diamond-drilling campaign scheduled for late fall 2026. Management also completed a North Shore / Baie-Comeau site visit assessing port, road and logistics infrastructure.

-29 June: The company mobilized field crews to Lac Guéret South, commencing field exploration on Zone 13 (a newly identified kilometre-scale EM anomaly) plus Zones 1, 4 and 6 (Zone 6 has returned high-grade intercepts in prior drilling); results will directly inform fall drill targeting. It also relaunched its website (fcgraphite.com).

-Context: the flagship Lac Guéret South Project (formerly Berkwood) holds a Zone 1 NI 43-101 resource of 1.76 Mt indicated at 17% Cg and 1.53 Mt inferred at 16.4% Cg, sits on a 167 km² land package adjacent to Nouveau Monde Graphite’s Uatnan project, with >$10M invested and funding in place to advance through 2026 toward a PEA.

ESGFIRE view (updated):

After a quiet, IR-driven May, June delivered exactly the hard exploration catalysts we said the thesis required: a defined two-phase program and, by month-end, boots on the ground on real EM targets, with a fall diamond-drilling campaign now the clear next milestone. This remains an early-stage critical-materials position with no near-term cash flow, and the thesis still rests on the resource quality, the size of the land package and graphite’s strategic role in North American battery supply chains – not on this quarter’s numbers. But the setup improved materially: there is now a dated path from geophysics to drilling. We stay patient, and watch surface results and, above all, financing discipline into the fall program.

Non-public investment portfolio – Events and important updates

ESGFIRE holds positions in the following private companies. We summarize any recent developments; if none, we note the latest known information.

Ola Media

Status in June: No material public updates in June 2026.

Latest public datapoints: Latest disclosed information (2025) indicates development of a digital advertising platform linked to EV infrastructure.

ESGFIRE view: Unchanged. We continue to monitor for commercial pilots or a funding round. Execution risk remains, but the model is aligned with the build-out of the EV ecosystem.

Alchemy

Status in June: Starts trading July 13th on the TSX V!

Evanesce Packaging Solutions

Status in June: Unchanged – no material public disclosures in June 2026 (latest disclosed company information remains 2023–2026, most recently a spring-2026 CEO interview).

Latest public datapoints:

Vancouver-based Evanesce manufactures certified-compostable, plant-based foodservice and packaging products built on its patented StarFybr Molded Starch Technology (upcycled plant/waste-biomass materials, home-compostable, decomposing in 90 days or less, free of PFAS and BPA), with production at its Early Branch, South Carolina facility. CEO Douglas Horne has publicly emphasised a licensing-led scale-up model built around cost-competitiveness with conventional packaging.

ESGFIRE view:

Unchanged. Evanesce operates in a structurally attractive market – cost-competitive compostable packaging into a sector facing accelerating single-use-plastic regulation. We continue to monitor for commercial scale-up and financing progress.

ESGFIRE watchlist – June 2026 performance snapshot

Our watchlist is a curated list of promising, undervalued companies that we follow closely. These names are not necessarily portfolio holdings, but we monitor them for potential entry.

EVgo (EV fast charging network NASDAQ: EVGO)

Business: Operates one of the largest public fast-charging networks in the U.S.

Key June catalyst: No major company announcement in June – the most recent material news flow remained Q1 2026 results (May 5) and a mid-May Chief Accounting Officer appointment.

Interpretation: A quiet month leaves the May setup intact: record Q1 revenue and the amended ~$750M DOE facility directly address the biggest bear point (how the capital-intensive build gets funded), but the soft Q2 revenue guide kept the shares under pressure. We keep EVgo high on the list as a clear infrastructure-execution story and want scale to translate into improving unit economics and a firmer near-term revenue trajectory.

Revolve Renewable Power (distributed renewables developer TSX-V: REVV)

Business: North American owner, operator and developer of renewable projects, with a development pipeline now exceeding 3,000 MW.

Key June catalyst: On 4 June (announced 8 June), Revolve signed agreements to acquire a ~125 MW U.S. utility-scale solar development portfolio – Henry (Illinois, 30 MW), Columbus (New Mexico, 56 MW) and Endeavor (Wisconsin, 39 MW) – each with site control in place, funded from existing resources and expected to close in June. The acquisition lifts the total development portfolio above 3,000 MW. Beacon Securities’ Kirk Wilson (June 9) reiterated a catalyst-rich view, flagging a potential sale of the 130 MW EL24 Mexican wind project and the Bright Meadows (Alberta) buildout.

Interpretation: Continued disciplined pipeline expansion into the strongest demand backdrop U.S. renewables have seen in years (data-centre and AI-driven power demand). The February US$40M Callaway facility gives Revolve financing visibility that development-stage peers usually lack; the market still under-rewards the stock on liquidity and small-cap sentiment, which is exactly why it stays high on our list. Next, we want ready-to-build milestones converting into project sales.

Electrovaya (lithium-ion batteries NASDAQ: ELVA)

Business: Develops proprietary lithium-ion battery systems for industrial and energy-storage applications, with expanding U.S. manufacturing.

Key June catalyst: No company press release in June, but on 5 June Roth Capital’s Craig Irwin raised his price target to $20 from $12 (Buy) after visiting the Jamestown, New York facility, arguing the plant could be sold out by end-2026 and highlighting new niobium-oxide cells (high-rate 10C charge/discharge) aimed at data-centre applications, with sampling underway and material volumes expected in 2027.

Interpretation: Fundamentals remain the clean part of the story – a profitable industrial-battery business growing revenue while staying in the black – and sell-side sentiment is improving. Yet the shares still softened with the broader small-cap/tech pullback in June. That is the execution-versus-quote gap in miniature; among watchlist names this stays one of the cleaner “profitable industrial battery” stories. We watch the Jamestown ramp and order timing.

Greenlane Renewables (biogas upgrading systems TSX: GRN)

Business: Supplies biogas desulfurization and upgrading systems for renewable natural gas (RNG) production globally.

Key June catalyst: The main June item was the Annual General Meeting (24 June), at which all directors and resolutions were approved; there were no new order or contract announcements in the month.

Interpretation: An administrative, low-news month after May’s step-up (the Panasonic do Brasil localisation agreement and the +36% Q1 revenue print). The question we keep asking is unchanged: order intake and backlog conversion into recurring, higher-margin revenue. We watch for the next system-sale contract to move that conversation forward again.

Veritone (AI software platform)

Business: Provides enterprise AI and data solutions through its aiWARE platform, Veritone Data Refinery (VDR) and Data Marketplace (VDM).

Key June catalyst: No major dated company announcement in June that we can confirm; the story remains the VDR ramp guided from Q2 onward, the Oracle migration (initial storage payloads targeted for as early as August), and the path to operating profitability “as early as Q4 2026,” supported by the targeted 30% operating-expense reduction.

Interpretation: Still a textbook execution-versus-sentiment name. The named-customer progress (Google, NVIDIA and the Oracle agreement signed in Q1) is exactly the concrete evidence we want in an AI-data story, but consumption-based VDR and government contract timing make revenue lumpy and the stock high-variance. We watch the H2 VDR revenue ramp and tangible profitability progress before treating the narrative as proven.

Beam Global (off-grid solar EV charging NASDAQ: BEEM)

Business: Produces solar-powered EV charging systems (EV ARC™) and resilient infrastructure for energy security and smart cities.

Key June catalyst: On 2 June, Beam deployed six additional EV ARC™ systems for the City of Long Beach, California (four for city fleet operations, two at Long Beach Airport). Separately, Beam is relocating its California manufacturing and production to a new ~55,000 sq ft campus in Yuma, Arizona (corporate HQ stays in San Diego), targeting roughly $400,000 of rent savings in 2026 and ~$2.7M over the lease term to mid-2031, plus lower production costs. Sentiment context: a mid-May Freedom Broker downgrade to Hold (target cut to $1.50) on the weak Q1, and a tight cash position, remain overhangs.

Interpretation: Municipal and airport deployments keep the demand signal alive, and the Yuma relocation is a sensible cost lever heading into a higher-for-longer environment. But Q1’s 51% revenue drop and thin liquidity keep this firmly a “prove-the-backlog-conversion” story. We watch backlog-to-revenue conversion and the profitability inflection.

About us:

ESGFIRE is a Swedish investment company and research firm that focuses on companies with either an environmentally friendly service or product. ESGFIRE has a performance record of over 1000 % returns since 2018. By only investing in environmentally friendly companies, ESGFIRE have outperformed the major indexes for several years. We have a track record of over 1100 % returns since 2018 using our own proven method of identifying high potential ESG companies.

Contact details

Website: www.esgfire.com

CEO: Filip Erhardt

Email: Filip@esgfire.com

Telephone:+46701609605

Legal Disclaimer

The stock price development above was calculated by taking the opening price at the first day of the month and the closing price at the last day of the month.

This post is based upon reliable sources, namely regulated press releases from the company, as referred to above. Nevertheless, this post may contain interpretations, estimates, or opinions of the authors, or other non-factual information. If that is the case, this is continuously stated above. Furthermore, any projections, forecasts, or similar are explicitly stated as such. These projections, forecasts, or similar have been conducted based on EV/SALES multiple calculations.

The author holds shares and/or other securities of these companies and the relevant

companies may or may not have paid the author for content posted on this website. This

may impact the content on the website. Because of the above, ESG Fire urges the visitors to always analyze all the posts critically in an objective manner, e.g., concerning the reliability of the relevant source and of what constitutes the authors’ personal interpretations. The visitor is hereby reminded that the post does, as set forth in the Post, contain interpretations, estimates, or opinions of the authors. This post was written by Filip Erhardt , at ESGFIRE , published at July 13th , 2026.

Investing in stocks is combined with certain risks and it is possible to lose your entire investment. Our posts are made for Educational purposes only and are not to be interpreted as tips , financial advice or recommendations of any kind to either buy or sell any stocks.

Companies may or may not be paying us for content posted on this website