Aduro – a unique ESG opportunity

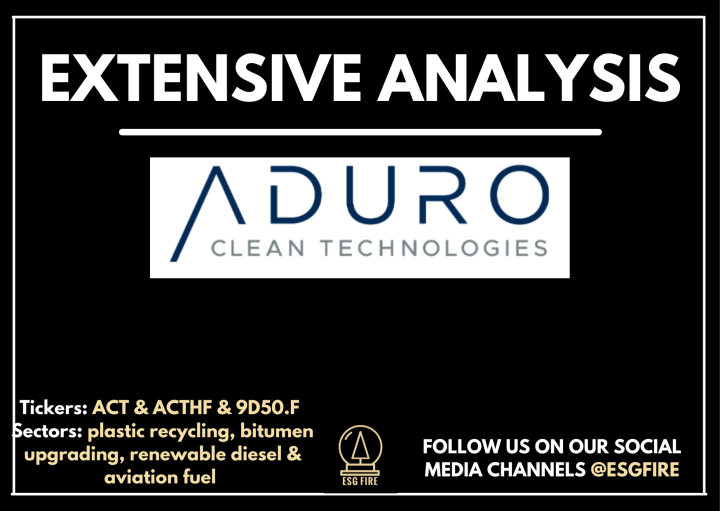

Company: Aduro Clean Technologies

Listings: CSE, OCTQB, FSE

Tickers: ACT, ACTHF, 95DO

Market cap at time of publication: 26 $ MCAD / 20MUSD

Stock price at time of publication: $0.75 CAD / 0.59 USD USD

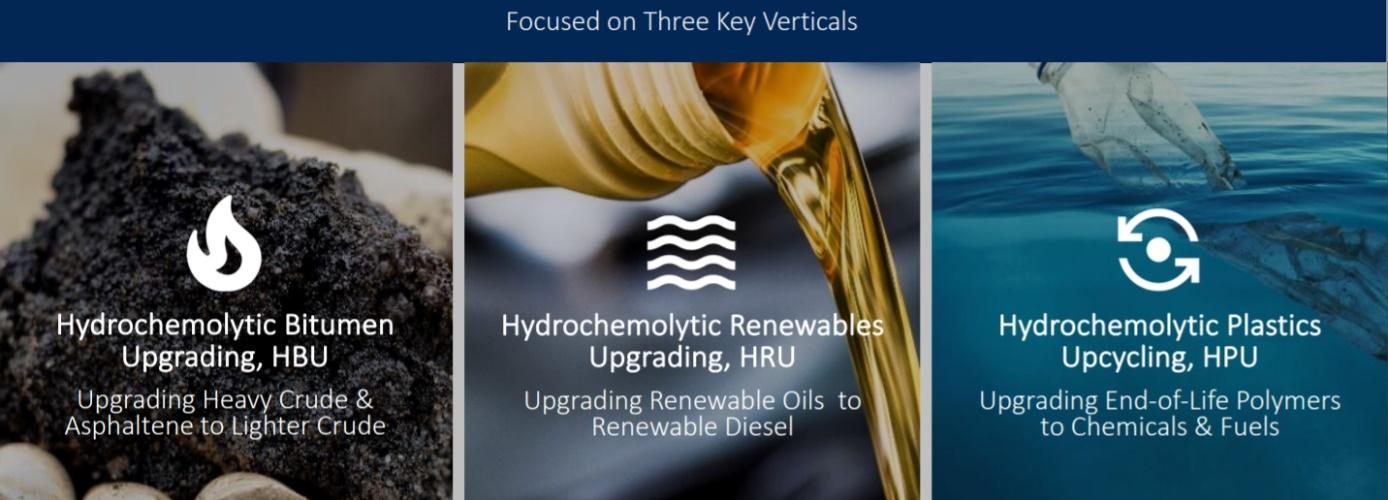

Business: Plastic recycling, bitumen upgrading, Renewable diesel & Aviation fuel

Website: https://adurocleantech.com/

Target price: See price target estimate at end of article

Comparable Peer evaluations:

Purecycle 674MUSD

Clean Energy fuels 1,25 BUSD

Agilyx 278 MUSD

Legal Disclaimer

We own shares of this company personally. Investing in stocks is combined with certain risks and it is possible to lose your entire investment. Our posts are made for Educational purposes only and are not to be interpreted as tips , financial advice or recommendations of any kind to either buy or sell any stocks.

Companies may or may not be paying us for content posted.

Short Summary:

Rarely do we come across investment cases that have the chance to change the world as we know it andbeing able to invest in such a company early is even more rare. Aduro Clean Technologies is a new addition to the ESGFIRE portfolio that has the potential to become a billion-dollar cleantech company with a new industry standard. The company has developed a patented, carbon neutral technology named Hydrochemolytic that can upcycle plastic, bitumen and renewable oils (Aviation fuel, canola, corn etc). The combined total global addressable market for Aduro’s three different market vetical is a staggering $437 billion USD. In fact simply looking at the domestic market in Canada for Bitumen upgrading this alone could be worth over $3 billion dollars. Aduro is now aiming to rapidly expand and commercialize their business with industry partnerships using a low capex business modelin order to maximise shareholder value. Aduro’s technology is necessary for a global circular economy! As a brief overview we want to highlight that Purecycle (which are further into commercial stage) and which focuses solely on recycling only one type of plastic (Polypropylene) in one of Aduro’s three possible markets is currently valued at 34 X of Aduro’s market cap. It should be mentioned that Aduro’s patented technology recently has received independent third party validation, which is something not many competitors can display ! Aduro owns all of their patents directly.

- See calculation below in the market overview section.

- https://ihsmarkit.com/research-analysis/canadian-oil-sands-diluent-demand.html

- https://adurocleantech.com/company-update/aduro-announces-achievement-of-first-milestone-after-receiving-independent-validation-of-hydrochemolytic-chemical-conversion-technology/

Another competitor, Agilyx from Norway is valued 14X of Aduro’s market cap with $30 MUSD projected revenues for 2022 . For the last 10 years management of Aduro have invested their own private funds to come up with a solution to some of the most concerning environmental issues faced by humanity today. The most environmentally hostile issues which Aduro addresses is how to unlock value from waste plastics that pollute lands and waterways all over the globe. The two other pressing issues addressed by Aduro’s technology include how to improve the characteristics of bitumen used in oil production through a greener conversion process (effectively eliminating the need for diluent and increasing the economic value of renewable oils (such as corn, canola etc) in scalable operations that can be implemented locally.

Hydrochemolytic (HTC)

HydrochemolyticTM (HTC) technology was originally developed to upgrade heavy oil. Aduro have since redirected and reconfigured their technology to upcycle plastics and upgrade renewable oils. Simply put the HCT technology leverages the unique properties of water in a chemistry system that transforms large molecules of low value into smaller molecules of higher value; materials with undesirable characteristics are converted into materials that are more useful, the result is a tremendous uplift in market value of the materials processed. Also ESGFIRE believes that one of the differentiating aspects of Aduro’s technology is the reduced reliance on hydrogen and less need for high heat in the process of cutting carbon bonds. This aspect both simplifies the processes and reduces CAPEX requirements tremendously. The time has now come for Aduro to commercialize this technology which ESGFIRE believes has the potential to become the new industry standard for upcycling worldwide. Aduro states that their technology is 50 % cheaper than traditional processes with lower expected CAPEX and OPEX. Aduro also states that their strength is their ability to scale their process to fit both large and smaller production requirements unlike the massive facilities required for economics by other competitors today. The company has cash at hand to keep their operations running for another 12 months ($150 000/month CAD burn rate) without external financing. Recently announced pilot facilities in Canada and Europe[4] could bring in revenue as early as the current calendar year of 2022. Warrants could also bring in an additional $1,5 MCAD.

Stock History background:

Aduro Clean Technologies was listed on the CSE on 29th of April at a stock price of 55 cents per share. Since then the stock price has increased moderately by 36 %. The market cap is right now hovering around 25-30 MCAD.

Ownership structure and incentives for management

Insider ownership: 16 million shares (35,5 %)

Free float: 18 million shares

Number of shares in the market: 34 million

Warrants / options: 15,9 million

Total share count fully diluted: 48 million shares

Extra shares granted to management if milestones are achieved: 26,7 million

Insider ownership in Aduro currently stands at a reassuring number of 36 % and there is currently a very tight free float of just 18 million shares. What really makes Aduro stand out in terms of ownership structure is the milestone system set in place to incentivise management to reach the official goals of the company’s development plan. We have never seen anything quite like this and think it’s extremely positive to this structure since it makes management interest even more aligned with shareholders. Most of the management’s upside is linked to hitting stringent milestones.

The milestones are as follows:

- A demonstration unit or showroom up and running and leading to commercialization with an industry partner which means a live pilot

2.A completed financial transaction with an institution which clearly has the capacity to finance Aduro majority owned commercial operation of a manufacturing plant producing Product for commercial sale. - Product produced by a manufacturing plant owned in part by Aduro where Aduro’s portion of the plant’s equity is at least $6,000,000 greater than Aduro’s investment;

- A third party entering into a licence agreement with Aduro in respect of the Technology which Aduro and such third party estimate will generate at least $15,000,000 in revenue for Aduro over a three year period;

- A third party equity investment in the Company of at least $9,000,000 at a company pre-money valuation of $120,000,000 or more.

- The total market capitalization of the Company remaining at or above $195,000,000 for 19 out of any 20 consecutive trading days;

- The Company having completed a public offering or private placement raising at least $12,000,000 at a minimum price per share of $1.05, or a combination of grants, $1.05 share offering and other financing transaction raising at least $12,000,000; or

- A third party enters into an agreement to acquire all of the issued and outstanding Company Shares at a minimum value of $3.00 per share.

The strike price for managements exercise of the 26,7 million incentive shares are at nominal value and the shares are all subject to a 3 year lockup period.

Technology overview

As previously stated the management team of Aduro have spent 10 years in R&D focusing on developing what’s called Hydrochemolytic technology (HTC) platform that has already been proven to work at lab stage level and the company has also successfully secured 7 patents (3 owned, 3 pending and one acquired) prior to going public. Management have so far invested over 4,5 MCAD of their own money while also securing a significant amount of non-dilutive funding via government grants during the process. Aduro describes their HCT as a water based chemical conversion platform that creates cleaner, greener resources for the 21st century from waste plastic, renewable oils, and bitumen. An important aspect which deserves to be highlighted is that “in recent lab runs, HPU produced 99% pure, diesel-like paraffin oil from polyethylene with a yield above 90%. Though the product could be used as fuel, Aduro CEO Ofer Vicus said the real prize within reach, thanks to HPU, is efficient chemical recycling of polyethylene (PE) for use in production of more polyethylene in a fully circular mode” . Aduro states there are competitors working on this solution as well but all of them currently use some form of pyrolysis which is limited at its efficiency at 76 % . All Aduro patents can be viewed HERE.

- https://www.forbes.com/sites/rrapier/2021/10/10/a-novel-solution-to-plastic-pollution/?sh=6c2dc66183c0

- Patents Assigned to ADURO ENERGY, INC. – Justia Patents Search

An important aspect that should be highlighted is that Aduro owns all of their patent and does not share any third party ownership of its intellectual property, also as previously mentioned the technology has been validated by an independent third party. The company aims to commercialize their product in three different verticals each with their own huge potential. The verticals which are being targeted are bitumen, plastics and renewables and are covered below in the market overview section.

In most cases, high temperature is used to crack down macromolecules and this process is referred to as thermolytic or pyrolytic. Aduro’s HTC technology on the other hand is a chemical conversion process that uses low value readily available metals as catalysts, the co-process biobased material also Glycerol, cellulose and other biobased materials replace the need for hydrogen gas.

HTC is a novel chemical conversion process that deconstructs macromolecules which are large, intractable molecule chains that are shortened in the processing operation to make them useful.

The heat levels required for the HTC technology is, according to management, considerably lower than comparable technologies which operates between 325 -350 degrees Celsius / 600-660 degrees Fahrenheit. Aduro’s processing does not require hydrogen gas which is a highly energy intensive source of energy which can also emit high levels of CO2 depending on the way that it is source

The HTC technology does however require bio-based material which is fed into the process and that becomes the equivalent of hydrogen in the chemical reaction. Another revenue stream which has not yet been highlighted is the fact that Aduro will be able to extract metals through the water stream that requires processing. The company plans to model this in full scale with their R3 scale up (processes 5-10 barrels per day) and with this they will have complete data on the full energy consumption process with its long duration trial.

The energy consumption required could be supplied with green energy from solar panels or a solar heat collector (ESGFIRE portfolio company Absolicon to name as one example ) for a 100 % green process. The HTC process does not use a significant amount of water since the wastewater from the process can either be returned back into the process or filtered and be returned to its source. Aduro have stated that they are very engaged in water management and want to contribute to a positive environmental impact.

Aduro’s technology is still at an earlier stage than some competitors which is also reflected in the extremely low market cap and valuation of the company which gives a tremendous upside possibility for early investors. As we have previously stated comparable competitors which are only active in ONE of Aduro’s three markets are valued between 10-34 times higher than Aduro’s current evaluation. Below is a summary of how far progressed Aduro’s technology is. NOTE even though the Bitumen upgrading is the only vertical closest to commercial stage these pilots will most likely be quite large and will be able to generate substantial revenues in the range of 4-40 million USD per year depending on scale (5000-50000 barrels per day pilots) and partnership.

Market overview

- https://www.forbes.com/sites/rrapier/2020/06/06/estimating-the-carbon-footprint-of-hydrogen-production/?sh=5bff11b524bd

- https://www.absolicon.com/

The global market for Aduro’s verticals exceeds $437 billion USD (307 B$ Biofuels, 63 B$ plastics, , Oil 67 B$)

The combined total addressable market for Aduro’s three domestic markets in Canada alone is 95 billion USD. Breakdown of the addressable domestic markets are as follows:

Waste plastics $30B

Renewables $25B

Heavy oil $40B

Market estimates above only calculate the domestic Canadian market.

Plastic recycling market

The plastics recycling market is most likely the most competitive one that Aduro is pursuing. Aduro’s HTC technology is a chemical deconstruction process that rapidly converts various kinds of plastic into components useful for a variety of consumer applications, for fuel, and even for true chemical recycling that produces new, virgin plastics. Every year mankind produces 370 million metric tons of plastic. Out of this only 14 % is actually recycled. An astonishing and shocking fact we ran into researching Aduro is that only 10 % of U.S. consumer plastic is actually being recycled. The EPA estimates Americans generated 292.4 million tons of trash in 2018. Twenty-three percent of it was recycled. Half of it ended up in landfills. If we break it down by material: paper and paperboard were 68% recycled. Glass, 25%. Metals, 34%. But plastics — only 9%. It should be noted that Aduro’s technology has been proved (in lab testing) to be able to process 6 out of 7 different types of plastics. Fortunately there are more and more government regulations aiming to increase recycling on a global scale.

- Biofuels Market Size Worth Around US$ 307.01 Billion by (globenewswire.com)

- https://www.globenewswire.com/en/news-release/2021/08/23/2284743/28124/en/Global-Plastic-Recycling-Market-Report-2021-Rise-in-the-Demand-for-Plastics-in-Diverse-Industry-Practices.html

- A new water-based solution for recovering add-on value from waste plastic – Canadian PlasticsCanadian Plastics (canplastics.com)

- PlasticsEurope & Ellen Macarthur Foundation

- https://www.epa.gov/facts-and-figures-about-materials-waste-and-recycling/plastics-material-specific-data

- https://www.epa.gov/facts-and-figures-about-materials-waste-and-recycling/plastics-material-specific-data

The European Union for example aims to increase plastics recycling to 50 % for 2025 and 55 % for 2030. Aduro recently posted a corporate video with a possible solution to clean our oceans this can be viewed by pressing here. Plastic, made from coal, natural gas and oil has historically been the most challenging commodity to recycle causing a global waste problem.

The plastics recycling industry is a highly fragmented market with many different types of competitors and processes. The plastic recycling market is experiencing a tremendous growth due to the global pollution of waste plastics and even more importantly is the consumer demand for recycled plastics over virgin plastics. Governments globally are imposing harsher and harsher demands for plastic recycling . Landfills are a global problem today which releases tremendous amount of harmful methane gases. Plastics in oceans is also a huge problem for the global ecosystem which threatens entire species. Higher cost of recycled plastics. Stringent competition with virgin plastics in terms of performance is a major factor restraining the growth of the market. China has recently banned the import of plastics that normally have ended up in landfills which has put a bigger pressure on western economies to find a solution to this pressing issue.

There are currently 7 types of plastics used globally, named from number 1 through 7. Typically type one and two generate the most revenue for recycling and the rest usually goes to landfills and incineration because its usually worthless. Most recycling facilities appear to only accept types 1,2 and 5 which could open up for a gigantic opportunity for Aduro if they can prove to, on a massive scale, recycle almost all types of plastics as their HCT technology potentially could.

The most commonly recycled plastics are:

1 – Polyethylene Terephthalate (PET) – water bottles and plastic trays

2 – High Density Polyethylene (HDPE) – milk and shampoo bottles

5 – Polypropylene (PP) – margarine tubs and ready-meal trays

Somewhat recyclable plastics (at specialist facilities) include:

- PlasticsEurope & Ellen Macarthur Foundation

- https://www.epa.gov/lmop/basic-information-about-landfill-gas

- https://www.nature.com/articles/s41467-020-20741-9

3 – Polyvinyl Chloride (PVC) – piping

4 – Low Density Polyethylene (LDPE) – food bags, protective foil

6 – Polystyrene (PS) – plastic cutlery

Some of these are incredibly hard to recycle plastics include crisp packets, salad bags, plastic wrap and more.

For more reading on the different types of plastic we found this write up useful.

Renewables oils aviation fuel & diesel market

The renewable fuels market , much like the plastic recycling market, is fragmented and contains many different stakeholders The burning of fossil fuels to create electricity, enable industrial production and to heat buildings stand for a majority of the worlds greenhouse gas emissions. Although Aduro is not in a near term outlook going to generate revenue from aviation fuel since this is time consuming and requires extensive testing with airline manufacturers it is a possibility for the future development. However, on the renewable diesel side Aduro’s technology may very well generate more near term revenues and therefor an overview of the market is desirable to comprehend the massive opportunity.

- Climate watch, the world resources institute (2020)

With the world population expected to reach 10,9 billion by the end of this century, up from 7,7 billion in 2019, we can only assume that global energy consumption will continue to increase. This combined with ongoing climate change which is increasingly becoming more alarming calls for immediate action in the renewable fuels sector. Electrification alone will most likely not be able to solve the replacement of internal combustion engines. Liquid and gas types of renewable fuels will be needed as well.

Even if the expected electrification of the transportation sector is very successful the most optimistic calculations show that oil is projected to fuel 20 % of the global transport sector in 2050. In the most pessimistic calculations however oil stands for 83 % of all global transport in 2050. There is currently an annual market of 900 billion gallons (or 3400 million litres) for renewable fuels. In a net zero scenario there will still be a 245 billion gallon (or 946 million litres) market demand in 2050. There is therefore a large market that needs to be addressed no matter how fast the global electrification is done and this gives room for plenty of companies, of which Aduro could be one.

Bitumen market:

Today there is a global oil production of over 98 million barrels per day. Canada represents 6 % of this production or roughly 5,88 million barrels per day. The need for diluent in Canada alone is estimated to be used in 2 million barrels of oil production per day. Diluent costs roughly 12-15 dollars per barrel and it’s a conservative estimate that Aduro would likely be getting roughly 20-30 % of the cost savings from diluent as a license fee. As an example, if Aduro is successful in taking just 10 % of their domestic market in Canada for their bitumen upgrading they are looking at annual licensing revenues of $160 million USD – $240 million USD for Canada ALONE. If we hypothetically assume Aduro would be able to conquer 1 % of the global bitumen market this number would likely be closer to $850- $1270 million USD in annual licensing revenues. Other aspects which make it highly likely that oil companies would not be deterred by this new technology is the fact that the process can be added without production halts and without interruptions. As the payback time for the technology is roughly 3-8 years this would be a quick payback and value adding feature for oil companies.

- https://ourworldindata.org/future-population-growth

- https://eu.usatoday.com/story/news/nation/2021/08/09/climate-change-reports-5-most-alarming-findings/5535699001/

- BP Energy Outlook 2020. Reflects Business-as-usual scenario

- BP Energy Outlook 2020. Net Zero scenario assumes that global carbon emissions fall by over 95% by 2050 broadly in line with a range of scenarios limiting temperature rise to 1.5 degrees Celsius. Net Zero

- https://ihsmarkit.com/research-analysis/canadian-oil-sands-diluent-demand.html

oil industry is not known for being particularly innovative however Aduro have strong industry connections that should prove valuable for a quick adoption.

Diluent is required to transport heavy oil in pipelines. Diluent is expensive and consumes valuable pipeline space. Diluent is used to partially upgrade heavy oil. Approximately 75% of all crude produced in Canada is exported to the U.S. (much of it heavy oil) therefore a bitumen upgrading product like Aduro’s would be a gamechanger if applied since it would free up a lot of pipeline capacity. Bitumen which is extracted from oil sands is a heavy petroleum that contains large fractions of complex long-chain hydrocarbon molecules. Depending on the process used, the bitumen product can sometimes contain as much as 2% water and solids, which does not meet pipeline specifications for transportation over long distances. Pipeline specifications can be met by either upgrading or diluting with a very light oil. Currently, about 65% of bitumen produced from the oil sands is diluted, typically with natural gas condensate, and sold directly to refineries as a heavy/sour blend.

The remaining 35% is upgraded into a light synthetic crude before being sold to downstream refineries. Most upgraded bitumen is sourced from oil sands mining operations, while most diluted bitumen is sourced from in-situ facilities. Diluent is used to upgrade oil in order for it to be transported via pipelines. Usually the cost of diluent ranges from 10-15 USD per barrel of oil which is a significant cost saving that Aduro could enable if their technology was to be used . Aduro’s technology would also be able to lower the carbon foot print of the oil process itself . Upgrading is therefore a process by which bitumen is transformed into light/sweet synthetic crude oil (SCO) by fractionation and chemical treatment, removing virtually all traces of sulphur and heavy metals. About one-third of Alberta’s bitumen is upgraded into SCO before being sold to downstream refineries. Looking at Aduro’s domestic market in Alberta, Canada about 35% of Alberta’s bitumen, mostly sourced from mined oil sands, is upgraded into light/sweet synthetic crude (SCO) before being sold to downstream refineries.

Competitors

Aduro states that their process has competitive advantage compared to their peers for several reasons. Firstly their CAPEX requirements are significantly lower, secondly many competitors solutions are only economically viable on a massive scale, thirdly competitors high operating temperatures require high energy input and often cause high CO2 output and last but not least competitors processing often result in complex product mixtures, often requiring postprocessing.

Since Aduro are operating in three different markets there is an enormous amount of comparable peers and competitors. For the sake of simplicity we have chosen to focus on a handful of competitors in each market segment therefore we do not claim in any way that this competitive analysis is a complete overview of the existing competition.

One thing that most competitors do have in common is that they are significantly higher valued than Aduro despite not all of them being significantly further advanced commercially. Aduro’s market cap of $20 MUSD stands out as miniscule when compared to industry peers.

Plastic recycling market competitors:

Purecycle Technologies

Market cap: $674 MUSD

Website: https://purecycle.com/

Listing: Nasdaq, USA

Purecycle commands a $674 MUSD market cap and focuses on polypropylene recycling only (type 5 plastics) . The company went public through a SPAC merger with Roth CH Acquisition I Co. (“ROCH”) in early 2021 which valued the company at post-money equity value of $1.2 billion.The company projects revenues of 6 million USD in 2022 and 176 MUSD in 2023. The company aims to build their own processing facilities across the United States which will require a significant amount of CAPEX. Their recycling process aims to produce only one type of plastics namely type 5 Virgin-Quality polypropylene. The company is currently ramping up production scalability and are opening new facilities. They use a highly CAPEX intense business model.

Company: Agilyx

Market cap: $272 MUSD

Website: https://www.agilyx.com/

Listing: Merkur Market, Norway

Agilyx has developed a technology for chemical recycling of post-use plastics known as depolymerization technology that handles Plastic-to-Plastic, Plastic to-intermediaries and Plastic-to-Fuels) and they also aim on a circular economy for the handling on waste plastics. Agilyx appear to have the most similar business model to Aduro as they are focusing on diversified revenue streams from technology license fee’s,equipment sales operating royalties and feedstock service fees. The company projects revenues of 13 MUSD for 2021 and 30 MUSD for 2022. Agilyx is in fairly early commercial stage with revenues starting to take off. They have 17 patents and a total of 150 M $ invested in their technology. They also have a few impressive partners such as Mitsubishi chemical and Exxonmobil ( which owns a 25 % stake in a joint venture) . It’s unfortunately unclear which types of plastics Agilyx can process, some documents indicate they can handle all types but this information is not clearly stated .

Renewable fuel market and aviation fuel competitors:

Company: Quantafuel

Market cap: $464 MUSD

Website: https://www.quantafuel.com/

Listing: Merkur Market, Norway

Quantafuel upgrades plastic waste into valuable products that are in high demand. Quantafuel claims to convert almost all kinds of plastic waste into environmentally-friendly fuel and chemicals.

Their entire value chain is circular, and production takes place by means of chemical recycling at Quantafuel’s facilities. The company projects 10 MUSD in revenues for 2021 and 30 MUSD for 2022.

Seeing as their SKIVE plant is not yet in full production it’s hard to estimate if their financial projections actually will be correct. They have yet to achieve proof of concept for some of their technology and recently had to announce a $45 MUSD raise.The company is also planning an expansion of their KRISTIANSUND plant. They are currently testing a pilot reactor for chemical line which is processing plastic waste and producing chemicals with promising quality. The company also has a big plant in ESBJERG for plastic sortings. One of their advantages is that they can process impure plastics and different colors. It’s unclear if Quantafuel can process all types of plastic or just some.

Company: Gevo

Market cap: $589 MUSD

Website https://gevo.com/

Listings: NASDAQ

Gevo is a good example of a competitor which is aiming to commercialize what they call the next generation of renewable jet fuel, gasoline and diesel fuel that they state has potential to achieve zero carbon emissions. Gevo projects $4 MUSD in revenues for 2022 and 15 million for 2023. Gevo does have an impressive portfolio of contracts and off take agreements. However its questionable whether its actually sustainable to use farmland and food crops such as corn and soy beans for fuel especially when looking at the growing global population and global food shortages. The price for food crops is also likely to increase which risks to undermine profit margins . Also Gevo have high CAPEX requirements for their facilities. The company does have an interesting production line of renewable natural gas.

Company: Lanzajet

Website: https://www.lanzajet.com/

Privately owned

LanzaJet’s technology is uniquely able to produce up to 90% of its fuels as SAF, with the remaining 10% as renewable diesel. The company was was founded through contributions Lanzatech, Suncor, Mitsui, along with support from ANA. They have recently also added Shell and British Airways as investors. Lanzajet claims that to have Agreements for 100% of offtake already in place. They also state that their sustainable aviation fuel is price competitive with conventional jet fuel when factoring in available incentives and the cost of carbon. They use waste-based, sustainable ethanol – that is not made from either food or feed as feedstock for their sustainable aviation fuel. Their goal is to reach 100 million gallons per year in commercial production by 2025. Lanzajet states that their fuel has been shown to reduce greenhouse gas emissions by at least 50% and up to 85%.

Company: Neste

Market cap: $29 BUSD

Website: https://www.neste.us/

Neste is a serious and massive producer in the renewable diesel sector. They state that their renewable diesel has up to 75% lower GHG emissions and reduced tailpipe emissions compared to fossil diesel. It’s not unlikely that a big actor like Neste could possibly be interested in licensing Aduro’s technology should it prove to be better than current manufacturing technology in the renewable diesel sector.

Bitumen Market competitors:

Company: Fractalsys

Privately owned

Website: https://www.fractalsys.com/

Fractalsys develops patented and cost effective solutions for transporting heavy oil and bitumen. They state that their products can “improve bitumen product quality and significantly lower bitumen viscosity allowing processed fluids to move more freely in transport pipelines at a significant cost advantage over alternatives”. They also state that their technology lowers greenhouse gas emissions with their enhanced jetshear product. Shortly put it their product reduces diluent need by 61 % which reduces costs, lower pipeline tariffs, lower quality discounts, opens up pipeline utilization and improve the ESG performance (11 % lower GHG from well to tank) . Fractalsys claims their product adds 14 CD of value to every barrel of oil processed. Fractalsys also claims there is a potential carbon credit feature with their product. If Aduro’s bitumen upgrading can perform as described by their company their technology is vastly superior to Fractalsys as Aduro aims to completely eliminate the need for diluent. Fractalsys is currently targeting a 54000 barrel per day production and have so far processed 225000 barrels of oil.

Company: MEG energy

Market cap: $4.5 BUSD

Website: https://www.megenergy.com/

MEG energy is an oil company which have developed a technology called Hi-Q.

The technology is a pipeline product with several advantages over partial upgrading by delayed coking. The product gives a high liquid yield (90%) without needing a catalyst. It also reduces the need for hydrogen and thereby decrease operating costs. Finally the technology also claims to give lower greenhouse gas emissions and a higher quality product. MEG have stated they may license this technology to other oil companies and if so it would be a direct competitor to Aduro’s bitumen upgrading.

Business model

As stated Aduro’s processing units cost anywhere from $10m to $50M and has a payback period of 3-8 years which is a significant improvement over current conventional CAPEX projects. We believe the company will have one or more revenue generating pilot projects to launch during the current calendar year of 2022. The three main revenue streams that ESGFIRE had identified for Aduro are likely licensing per volume fees, joint venture projects and equipment sales.

Aduro is at an early stage in their commercial phase which means they will most likely be flexible in terms of business models to maximise shareholder value. The business models for bitumen upgrading will likely look different than for plastics upcycling. The licensing revenue model offers the option to work with Engineer Procure & Construct companies who often already have a large client base that they are already servicing. These companies are constantly looking for new technology solutions. The licensing model will likely generate revenues for Aduro in the term of sharing cost savings and with a 20-30 % cut for the company.

For joint venture projects, similar to how competitor Purecycle operates, would involve the design , construction and management of a facility. Here the feedstock supply and offtake are aligned and involves an extended producer responsibility. This may become a model that producers will start having a closer look at. Lastly Aduro may engage in straight forward equipment sales however we do not believe this business model will be the priority for management at this stage. We think licensing will be the main revenue model for Aduro to begin with.

The plastic recycling market is the one for which Aduro is building out their test site in Sarnia Ontario for. Our impression is that it seems their goal is to find a homogeneous supply source at this point rather than municipal waste.

Risks associated with an investment in Aduro Clean Technologies

This risk section addresses some of the most obvious risk with an investment in this company. We do not claim to have addressed all risks associated with this investment case.

Technology risk

If Aduro’s technology does not prove to be able to deliver results as good as previously presented or if the technology for some reason does not work as intended on one or all verticals it could pose a significant risk for the company’s existence. What speaks against this risk is the fact that the technology has been developed during 10 years, has been patented and has been proven to work at lab stage level and now also has third party validation. Still this is a risk investors need to consider.

Financing risk

Currently Aduro is funded for the next 10-12 months. The company currently has a low burn rate of about 150 000 CAD per month . The company will surely need additional financing within 12 months which may cause dilution for shareholders. However thanks to their business model of primarily going after licensing revenues and joint Ventures this should prove not to cause as big of a dilution effect as if the company was pursuing a business model where they aimed to own all operating facilities.

Competitors copying technology

There is a risk that competitors may try and reverse engineer or simply copy Aduro’s unique technology. The company have successfully secured 7 patents (3 owned, 3 pending and one acquired) prior to going public yet this is a risk investors need to be aware of. It could also pose as a litigation risk if expensive legal processes take place when Aduro defends their patents from intrusion.

Management risk

Aduro is by any measurements a small company with a close circle of leading management members. The risk of losing one of several members of management and thereby valuable knowledge has to be addressed. Current management have significant insider ownership therefore it’s unlikely they would be headhunted to a competitor but it’s not an impossible scenario.

Market adoption

As with all new technology there may be resistance from users in adoption. If Aduro has a difficult time finding early adopters for their technology it could pose a significant risk in their ability to generate near and long term revenues. Aduro’s success will be dependent on their ability to find early adopters and to bring these onboard as customers.

Management overview

The management team of Aduro is very experienced in the aspects of chemical engineering , renewable energy and business development. The team have diverse experiences that should benefit the company’s development.

One aspect investors definitely should consider is that no one at management level earns an average salary more than $45 000 CAD salary per year. In fact, both the CEO and CTO did not pull any salary historically in and had to record a salary as part of being a public company. It’s not unusual to see management in public companies raise their salaries enormously once the company goes public and therefore its quite intriguing to see that Aduro had chosen a very different approach with lower base salaries and a milestone system that aligns very well with all shareholders’ interests.

Upcoming catalysts for Aduro Clean Technologies

Below is a summary of upcoming catalysts which may have an effect on the evaluation of the company. It is by no means a complete list.

Buyout candidate

There is no shortage of billion dollar companies searching for feasible clean technologies to adapt in their business. As Aduro’s technology can be applied on three different verticals it could definitely prove to be a buyout candidate for larger corporations or SPAC companies.

Technology disclosure

Since the details about Aduro’s technology have not yet been revealed we are hopeful that the market will see more information on the technology soon from the company which will reveal the true value across all markets. Hopefully this disclosure will also bring into light which potential partners Aduro are considering in all three market segments.

Demonstration of showroom

Aduro is planning to utilize the Showroom unit to run client trials and demonstrate the technology and its capabilities to future clients. The demo unit will initially be used for heavy crude oil, followed by various plastic materials.

Revenue generating Pilots

We are hopeful that within 6-12 months we will see one or several revenue generating pilots for Aduro. This could either be with their bitumen upgrading or with their plastic upcycling.

Since the technology adds value and is cost effective even at smaller scale we think these pilots will add meaningful revenue to the company.

Aduro announced that over the past 12 months they have been in discussions to form a partnership with Brightlands Chemolot Campus. “The objective of this partnership is to complete an installation that applies Aduro Hydrochemolytic™ technology (HCT) to demonstrate, on a tons per day scale, the conversion of polyethylene (PE) waste to useful feedstock for chemical processes. Interest in this project by Brightlands is a result of its comprehensive and detailed review of HCT. The review concluded that HCT offers distinct advantages over traditional pyrolysis for bringing PE into the circular economy through chemical recycling to obtain valuable, high-purity products, such as value-added chemicals or feedstock for the production of new, virgin PE.” This review by Brightlands is a strong indication of support that the chemistry works and is novel. Brightlands has played host to some of Aduro’s competitors including Plastics Energy Itero & Quantafuel

Aduro also recently announced a collaboration with Switch Energy a business involved in the collection and processing of agricultural waste plastics and films. This is an example of feedstock that can be collected and returned to the circular economy rather than ending up in landfill or polluting farmers’ fields. We think this is the right size to scale up and prove the commerciality of the technology. Again they have moved toward identifying and engaging industry partners despite not having published the results of the first Milestone. A testament of the validity of the technology and its advantages over existing approaches.

JV cooperations and licensing agreements

Long term (9-18 months) we are looking forward to seeing Aduro sign larger licensing and joint venture agreements across all three markets. Most likely we are anticipating that the plastics and bitumen market will be the first markets targeted by the company.

Price Target estimation

We must stress that this price target simulation is highly hypothetical and is only made to show the potential of the share price development, this should not be viewed as any form of guaranteed share price development.

Estimating a price target for a company of Aduro’s nature that has revolutionary technology is close to impossible. First of all because we do not yet have all the financial aspects of their business models on all three vertical markets and therefore it’s not possible to apply a traditional price to earnings ratio which is the most common valuation metrics used by investors.

One of the few ways to value an innovative clean technology company like Aduro is to look at price to sales multiples. If an investor takes the average price to sales (p/s) multiple of four main competitors of Aduro on their financial projections made concerning 2022 ( Quantafuel, 16 ,Purecycle 94, Agilyx 10,5, MEG energy 1,26) the average price to sales multiple would be as high as 30. However we do not find this number to be realistic. However a Price to sales (p/s) number of 10 would according to ESGFIRE be reasonable for a company of Aduro’s potential short term. Stretching this into an even more conservative angle we could assume that in 5 years the size of Aduro would make a P/S multiple of 5 more relevant since the most explosive growth can be presumed to be behind them. If we therefore assume that Aduro in 5 years would be able to take a market share of just 1 % of their domestic Canadian market in Canada valued at 95 billion dollars the revenue number would equate to a staggering $950 million CAD. With a P/S multiple of 5 this would imply a market cap of $4750 MCAD. This number is mind boggling but not unrealistic comparing to the evaluation of similar companies. Assuming today’s share count of 75 million and also by adding a 50 % dilution to take into account additional need of funding this would put the total share count in 5 years at 112 million shares. Applying our hypothetical 5 year projected market cap $4750 MCAD with a P/S ratio of 5 would give a price per share of $42,5 CAD / $34 USD. It should be highlighted that the domestic Canadian market for all three market verticals is valued at 95 billion USD but the global market for all three market verticals is valued at over $437 billion dollars.

Conclusion

Aduro is sitting at avaluation of just $26 MCAD / $20MUSD with three different markets that all have multibillion dollar potential. Investing early in cleantech is always a big risk but we view this risk as one we are confident in taking in the case of Aduro . Comparing valuation wise with for example plastics recycling competitor Purecycle that only handles one type of plastics and stands at an evaluation of 345 times higher than Aduro’s and whom currently have very low revenues makes a potential increase of 10 X valuation forf Aduro to $320 MCAD / $260 MUSD seem small in comparison.

Legal Disclaimer

We own shares of this company personally.

Investing in stocks is combined with certain risks and it is possible to lose your entire investment. Our posts are made for Educational purposes only and are not to be interpreted as tips , financial advise or recommendations of any kind to either buy or sell any stocks.

Companies may or may not be paying us for content posted on this blog.