Paul Andreola from Smallcap Discoveries conducted an interview during a twitter spaces session yesterday

20/2 2023 at 20.00 CET with Filip Erhardt from ESGFIRE which discussed smallcap investing in the ESG sector.

Below is a compressed version of the interview transcript which generated great interest among listeners.

-Hi Everyone and welcome to this Twitter Spaces session by myself Paul Andreola from Smallcap discoveries with Filip Erhardt of ESGFIRE.

Paul: Filip can you begin and tell people about your investing journey!

Filip:

Sure Paul, My background is as an entrepreneur with an HR law degree with experience from serving as manager and on board positions in different smallcap companies. I’ve founded different companies myself over the years and having worked in Investment relations, Business to business Sales and human resources it gives me a crucial edge when doing due diligence in small cap companies.

My journey in investing in stocks began over 15 years ago when I was a typicall smallcap stock picker and at the time I didn’t really pay much attention to any specific industry but was rather opportunistic in my approach.

Paul: Can you tell us about ESGFIRE, why you founded it and how you got to where you are now?

Filip:

ESGFIRE is located in Sweden, Europe. It was founded in 2018 because I saw a need to educate investors about the possibilities in ESG/cleantech smallcap investments. ESGFIRE so far have had returns of over 1100 % for the ESGFIRE portfolio. When I say we its because I have different advisors with different skills that helps me assess potential portfolio companies.

I had seen many dividend stock gurus talk over the years about how people could become financially free using their method. When starting ESGFIRE I wanted to show people that there is another sometimes quicker although riskier way in the form of ESG smallcap investing to become financially free ,if that is your goal that is.

ESGFIRE is therefore organized like an investment company but operates as an investment community.

The way it works is we have a 100 % transparency in our portfolio which is published on our website www.esgfire.com and it has a free newsletter attached to it. This means we have skin in the game compared to most other analyst firms or stock gurus that do not own stocks of the companies that they cover and analyze.

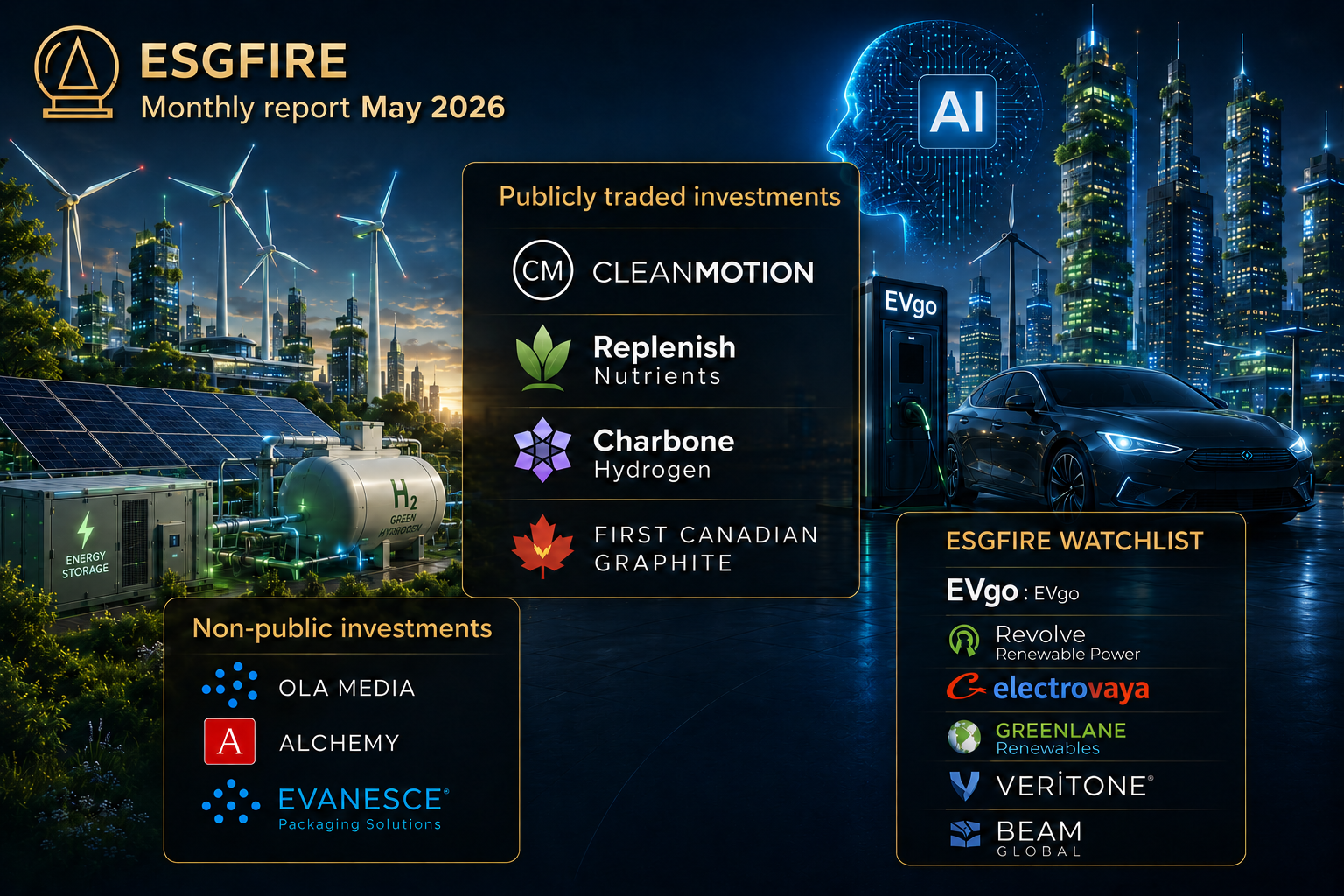

About 70 % of the portfolio consists of public companies and 30 % are non public companies which typically have 12-24 months until IPO . This gives our subscribers a very interesting deal flow. Currently we have 13 companies in total in the ESGFIRE portfolio.

For transparency we want to mention that we occasionally do get paid to write analysis and coverage of companies but we only choose to do so for companies in which we want to own stocks in ourselves meaning into either existing or new portfolio companies that we accept after careful due diligence. This is the case since our main business is to make good returns for the portfolio.

All our posts are automatically sent to our subscribers who then in turn can discuss our portfolio companies and other topics on our open and free discord channel. What separates us from other stock sites, analysts and investment companies , in my opinion, Is that we are 100 % transparent about changes in our portfolio and we have skin in the game. As soon as a company is either added or sold to the portfolio our readers are alerted typically the same day . We invest for the long term, we may occasionally trade within our positions but this is very rare and only in the event of either major positive or negative news.

Paul: Great Filip and why did you choose ESG?

Filip:

The reason I chose ESG was because back in 2018 I could see that the biggest positive macro trend with big tailwinds which would last for 20-30 years was in ESG and clean tech companies. The macro tail wind with initiatives from government, companies and consumers gives an enormous advantage for the whole sector in the ongoing green transition since a majority of companies and governments globally are working in the same direction.

Paul: So what is your edge in the area?

Filip:

My edge is now that I now have years of experience doing due diligence on ESG / cleantech small caps and know what to look for and what to watch out for. Having an entrepreneurial background I know what obstacles most small and growing companies are facing. Also having great advisors to discuss with strengthens the overall selection process.

Paul: What do you look for in your scope of investments?

Filip:

As of now the main scope of investing is profitable or at least very near breakeven small caps in the ESG/cleantech industry. In other words it has to be an environmentally friendly business product or service. If the company is not profitable it needs to have a high MOAT or uniqueness for us to become interested.

We have done some new investments recently into Agtech and the electric grid sector. These may not be what investors first think of when they hear ESG but they are definitely interesting and growing sectors.

Paul: How does the selection process work for ESGFIRE?

Filip:

Typically we look at close to a hundred companies to find one which we want to accept into the ESGFIRE portfolio, sometimes even more. If the company does not have competent people running it and has a clear path to profitability or a very high moat to competitors and is near breakeven, then it wont likely be of interest to us.

We want to see that management owns a large part and has skin in the game alongside with us. If they don’t then that sends a clear signal to us that they aren’t really entrepreneurs but more likely just officials / administrators.

We try to find undervalued, under analyzed , high potential and interesting companies which haven’t been discovered by the wider market yet. Typically, the competition among investors in this sector is fairly low still which gives us a big advantage and allows for us to come in at a good timing.

The different advisors we have on our team look at all investments before they are accepted into the ESGFIRE portfolio.

We also continuously evaluate the current portfolio companies and if we are not happy with the progress of the company, we will try to give input to the management team how to improve but if this does not occur we aren’t shy to exit to positions that are underperforming.

Paul: Great and what industry trends are you seeing right now that average investors may not be paying attention to?

Filip:

There are a few industry trends we would want to highlight the first being:

Ag tech companies

For those unfamiliar with Agtech its strives to make the agricultural system more efficient and streamlined through the application of a wide array of technologies, from the usage of AI to drones and robotics.

The sector also includes companies that are for example making environmentally friendly fertilizer and utilizing technology to raise crop yields in an envinronmentally friendly way . This could for example be autonomous robots that can be used on the crop fields along AI and gps/satellite technology and also vertical farming.

What we are seeing is that there are many very cheaply valued publicly traded ag tech companies in this sector which surprises us considering how the world drastically needs to increase food production in order to sustain the quickly growing global population.

Our belief is that the sector will start to see a premium valuation in the coming years much like companies in electrification has seen in the last few years.

VC firms have already acted on this trend. For example In 2022 797 AgTech startups globally raised $10.66B which from 2020 is a a deal value increase of more than 58% year-over-year from 2020.

One of the main reasons the sector finally seems to have become established with investors is the changing buying habits of millennials in particular and people in general when it comes to their food’s taste, nutrition and sustainability.

We also think that Russia’s invasion of Ukraine highlighted how vulnerable supply chains are globally which in turn has increased governments, consumers and companies awareness of the importance of locally grown and sourced food.

Secondly: Last mile delivery vehicle producers – an unknown market for most investors

For the European market alone there are currently 16 million light commercial vehicles mostly running on fossil fuel which will need to be changed into environmentally friendly alternatives such as electric and hydrogen vehicles.

One major market tailwind: In Europe for example there is a goal for the 100 largest cities to become climate neutral by 2030. Meanwhile in the United states we have the Inflation Reduction which provides tax and subsidy incentives of as much as 30 percent of vehicle costs to switch to electric vehicles.

This is why we have made a few careful picks in this sector. It’s important to be selective in this industry as not all suppliers will succeed but the ones who do are definitely going to be making a lot of good and money.

As a third pick: Investments in the power grid

As the world and Europe especially is becoming more and more dependant on electric vehicles this is putting a huge strain on the electrical grid and the distribution network.

The typical power grid is simply not built for a reality where everyone is driving an electric car.

There will be an increased risk of power outages and downtime in industries if the electrical grid in most countries is not maintained and expanded rapidly.

What we have learnt is that the Annual market for Investments in distribution network within EU+UK is expected to grow between 50-70 % from 26 billion EUR to 34-39 billion EUR. The increased budget has to do with ability to meet demand, integration of renewable resources, increased flexibility/ quality and digitalization. Due to this fact we are paying a lot of attention to companies which are active in this sector and who offer smart solutions in utility and storage.

As a fourth and final industry trend: Hydrogen and Clean natural gas engine component suppliers

As we have already discussed it’s a huge challenge to electrify everything in transportation and Electrification will likely not be the only alternative in the green transition. Higher overall prices in the last year for charging electric vehicles in Europe is in turn also a driver for this sector.

The suppliers we have looked at in the industry of Hydrogen and Clean natural gas engine components are currently valued mostly like any other OEM which means a roughly 8-12 times earnings. We think this is likely to change into a premium over the coming years .

One thing to keep in mind especially for the European market in this is the fact that The European Parliament recently has ruled that hydrogen made with France’s nuclear-powered electric grid will be classified as “low carbon.” This sets the precedence for hydrogen vehicles moving forward.

Paul: Thanks for these insights Filip, are there any traps investors should look to avoid?

Filip:

Definately, There are a trends and sectors for ESG investors to watch out for and stay away from right now:

Charging station suppliers:

We are staying away from charging station suppliers/producers since it’s become a cut throat market with extremely low margins. There is likely to be an extreme consolidation and bankruptcy trend in this market and it’s right now very difficult to know which company will come out on top in this sector.

Profitability is also a big concern for most companies in the sector. Not even all of the largest companies of the sector are profitable. The most profitable ones aren’t even seeing EBITDA margins above 20 % EBITDA .

Battery producers:

We are also staying away from battery producers as its right now highly uncertain which battery technology is likely to be the new industry leader in the coming years. Theres also a very big price pressure on battery suppliers to continuously come up with more efficient and cheaper solutions which is likely to give the sector a large research and development investment need for the foreseeable future.

Last note on ESG company trends to be careful of

It’s a new reality today versus 1-2 years ago when growth companies had little trouble filling private placements / equity financings . Money isn’t free any more due to higher interest rates and since it looks like it will still take some time for interest rates to come down in both Europe and the United States we have become wary of companies that are underfinanced and which are approaching stages where they may need additional equity financing.

This in turn makes it even more important to screen the major owners of companies that are likely going to be needing additional capital within the next 12-18 months. Weak majority owners is not a good recipe if you want to stay invested in companies with a financing need.

Paul: If you would mention a few stocks right now to highlight which would it be ?

Filip:

I’d say Clean motion a last mile delivery service vehicle producer, Landi Renzo a hydrogen play unknown to most investors, Absolicon solar collector , and Gomero in the power grid sector.

Paul: Thanks for joining us Filip and we hope to see you soon again!

Filip:

Thanks Paul it was a pleasure to be here!

Legal Disclaimer

We personally own stocks of the companies mentioned above.

Investing in stocks is combined with certain risks and it is possible to lose your entire investment. Our posts are made for Educational purposes only and are not to be interpreted as tips , financial advice or recommendations of any kind to either buy or sell any stocks.

Companies may or may not be paying us for content posted on this blog.